Challenging Your Investment Thesis: Eaton (ETN)

Consensus Thesis: A high-quality compounder to play the energy transition megatrend

Eaton is widely viewed as a high-quality industrial compounder, strategically positioned at the crossroads of:

· Electrification and grid modernization

· Data center and AI infrastructure buildout

· Aerospace recovery and mobility transformation

Investors are paying a premium for Eaton’s strategic positioning, management’s execution capabilities, and more importantly the belief that this growth is durable over the medium to long term.

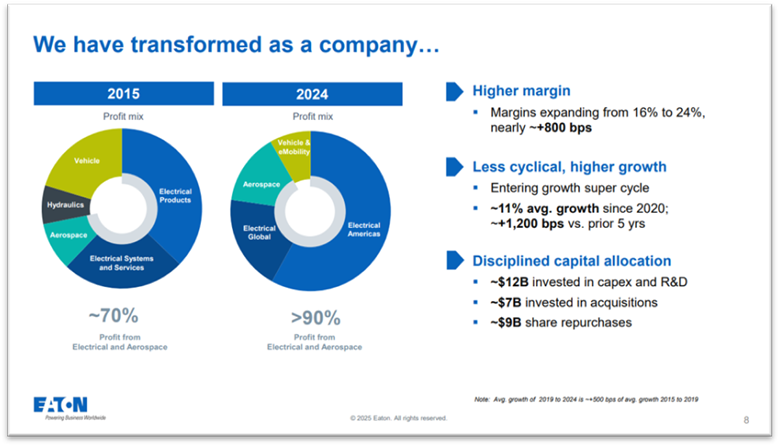

Eaton has significantly transformed its portfolio over the last decade and has now positioned itself as less cyclical and higher margin industrial

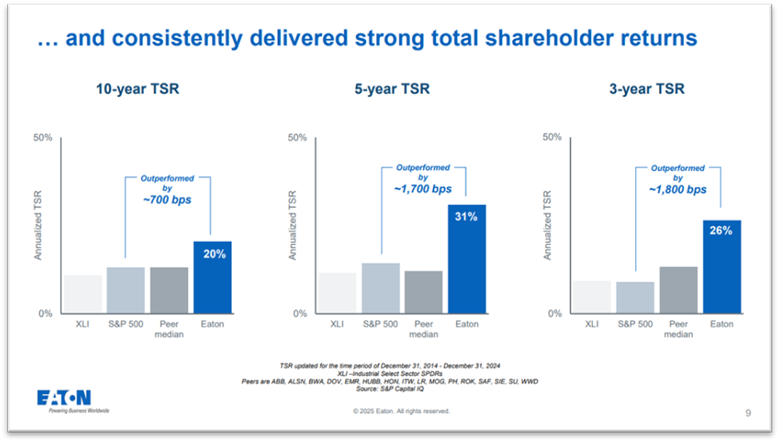

Strong underlying operational performance has also translated into industry leading shareholder returns

Reverse-Engineered Expectations: what is the market pricing in today?

Growth Longevity = Premium Valuation

The market is implicitly underwriting high-single to low-double-digit earnings growth through the decade, with stable or rising margins. This implies:

· The $1.9T project pipeline will convert steadily into high-margin revenue

· AI/data center capex will remain robust, not just in 2026, but through 2029+

· Electrification will drive global demand across geographies and sectors

· Operating leverage and pricing power will be sustained in a post-peak inflation world

In short, the valuation rests on a belief in duration-that Eaton's current growth trajectory is not cyclical, but structural.

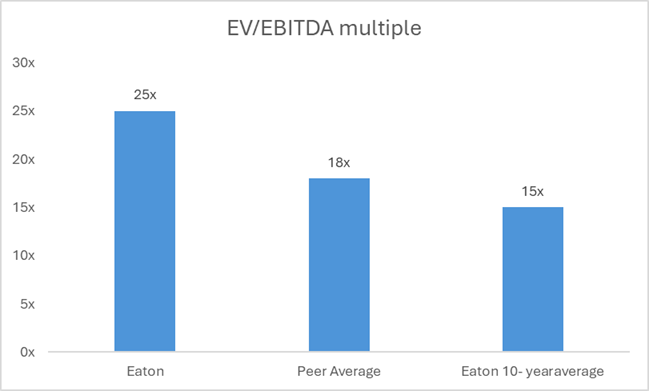

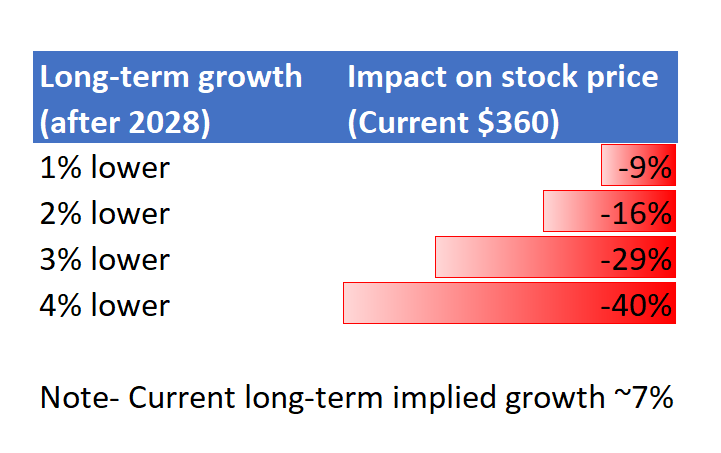

Valuation reflects this: Eaton trades at ~25x forward EV/EBITDA, well above historical and peer averages. It’s not about next quarter-it’s a multi-cycle bet.

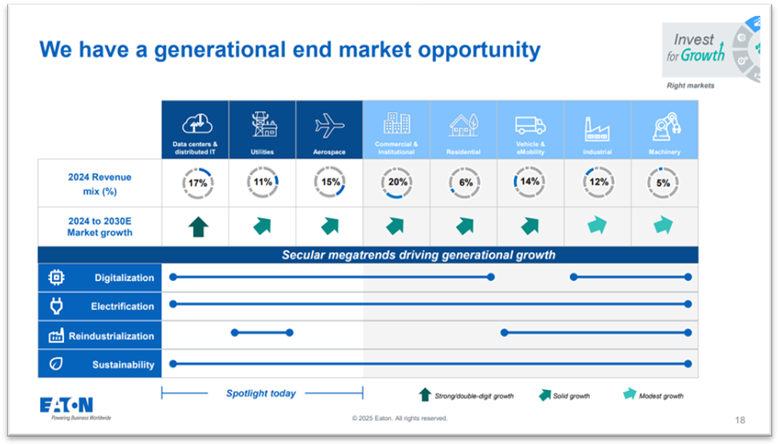

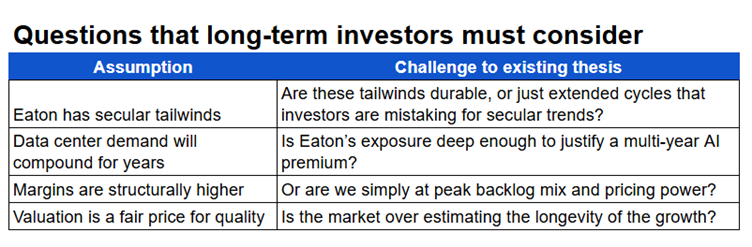

Yes, Eaton does have a generational end market opportunity- BUT the real question is how much of this can they reliably capture without busting their balance sheet and/or diluting their margins and ROIC?

Where the narrative may be vulnerable

1. Duration Risk: Growth Longevity is the key risk

The multiple isn’t just pricing next year-it’s pricing five years of visibility.

But in infrastructure and industrial cycles, visibility beyond 12–24 months is notoriously fragile.

- Risk: Even a modest pushout or slowdown in project starts or data center capex can challenge the long-term earnings glidepath

- Valuation Sensitivity: At ~25x EBITDA, Eaton’s multiple is acutely exposed to changes in duration assumptions

2. AI and Data Centers: Fully Valued, Narrow Exposure

Eaton is viewed as a key enabler of AI/data center growth but this is just ~15% of Electrical segment revenue, not a dominant driver.

- Crowded Trade: The entire electrification & power chain sector (ETN, Vertiv, Schneider, ABB) has been bid up on the same AI narrative

- Contrarian View: If AI spend normalizes (even temporarily), stocks priced for long-cycle secular demand may get hit the hardest

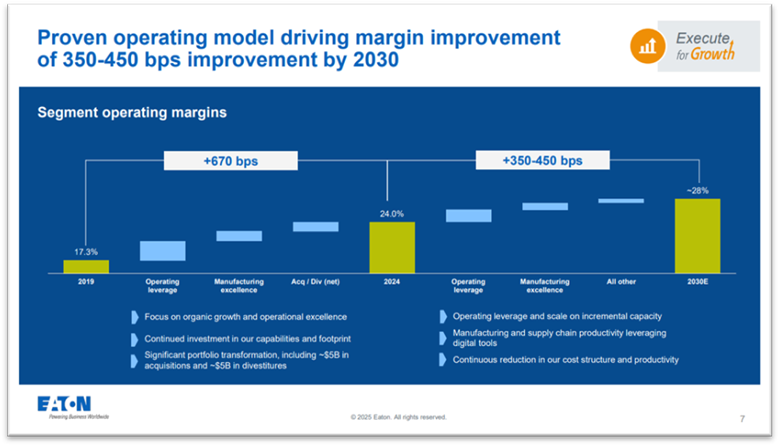

3. Margins are near the ceiling, not floor

Segment margins are at 24%-a record. But with cost normalization, backlog mix shifting, and pricing tailwinds moderating, the operating leverage story may be mature, not just beginning.

- Question: Can margins expand further without significant revenue upside?

- Risk: Any margin contraction even temporary undermines the FCF compounding thesis that underpins the multiple

4. Backlog ≠ Revenue

The $1.9T global megaproject pipeline cited by management is not contractual and includes speculative, government-linked, or pre-FID projects.

- Signal Risk: A flattening book-to-bill or backlog depletion without replenishment would raise questions about the assumed revenue curve

- Execution Risk: Supply chain friction, permitting delays, or political changes could materially alter timing and conversion rates

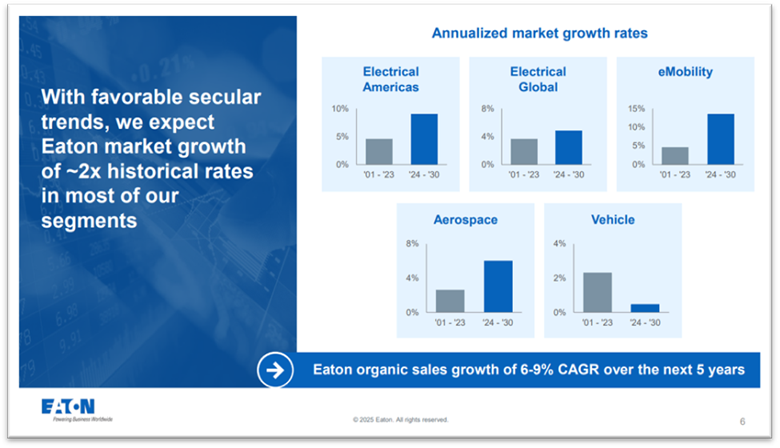

Eaton’s management is guiding for 6-9% organic sales growth- which in our view is very aggressive for an industrial company of this size.

Technical view on the stock

Would I go out and aggressively sell? Probably not! The technical set up still looks solid. The stock may see further strength once it takes out the recent high of $400. Its too early to start looking for shorting opportunities.

Final Thought

Eaton is a strategically advantaged industrial franchise with credible long-term tailwinds and solid execution. But the current valuation is a pure bet on growth duration-not just growth level.

If growth proves to be shorter, slower, or lumpier than expected, the stock’s re-rating could be swift.

Member discussion