Challenging Your Investment Thesis: Vertiv (VRT)

Consensus Thesis: A Pure-Play Infrastructure Winner of the AI Age

Vertiv is celebrated as a prime beneficiary of the data center and AI infrastructure boom. As cloud giants build out next-gen capacity, investors view Vertiv’s power and thermal management systems as mission-critical. The company has delivered strong order growth, expanding margins, and multiple upward earnings revisions. It’s now a top momentum name in the AI trade.

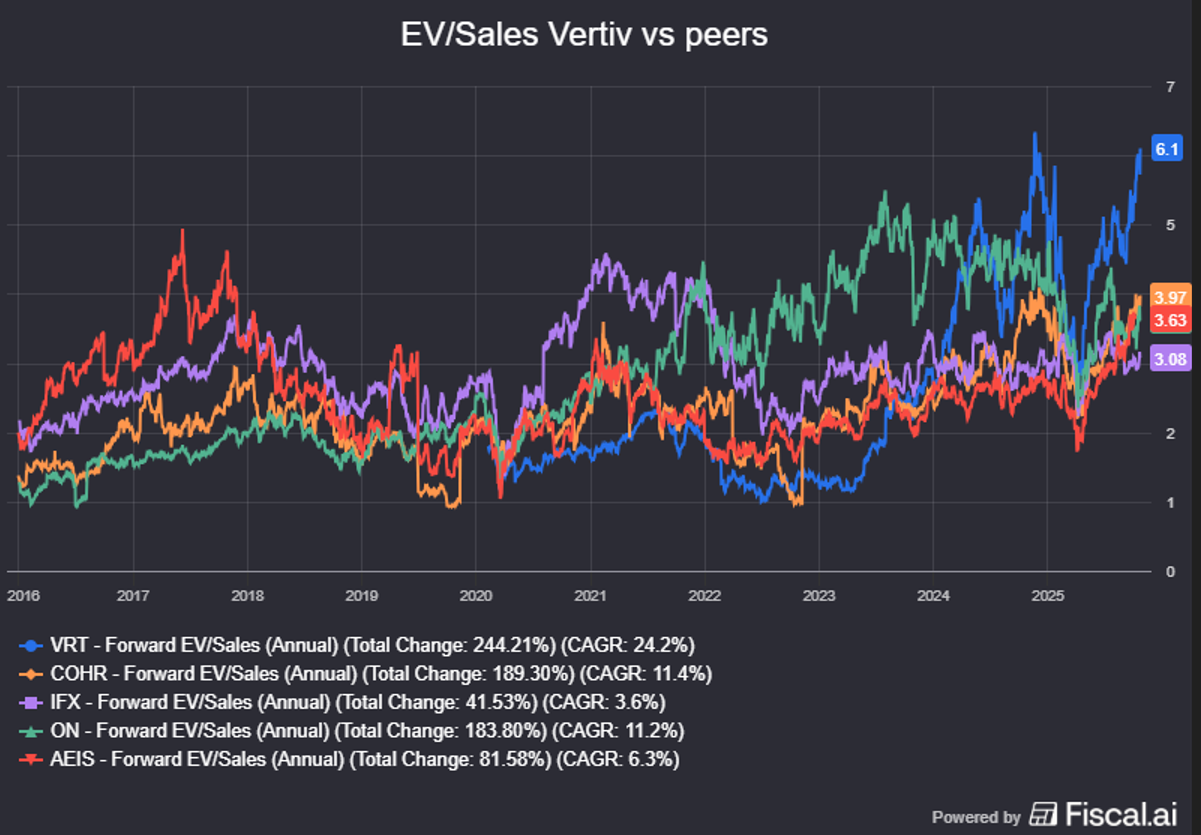

Valuation is steep-trading at 5x EV/Sales and 25x EBITDA but bulls argue this is justified by a multi-year secular growth runway.

The Embedded Assumption: Vertiv will remain a key enabler of the AI infra buildout

The current narrative assumes:

- Hyperscaler and colocation capex will remain strong and continuous through the decade

- Vertiv’s backlog and modular product lines (e.g., OneCore) will translate into profitable growth

- Vertiv will maintain its leadership despite rising competition and product complexity

- Margins can continue to expand with scale, supply chain localization, and mix shift

In essence, investors are betting not just on growth, but on its duration, defensibility, and scalability.

Where the Narrative May Be Vulnerable

1. New “Picks and Shovels” Narratives Are Constantly Emerging

In every tech cycle, the infrastructure story evolves. Vertiv’s role as a critical enabler may be compelling today, but market narratives shift quickly. Several new "infrastructure" themes are starting to attract investor attention:

|

Emerging Narratives |

Example Stocks |

|

Liquid

cooling tech for GPUs |

Subsystems

by Asetek, CoolIT (private), Nautilus |

|

Optical

interconnects & photonics |

Infinera, Coherent, Marvell,

Broadcom |

|

Specialized

power semiconductors |

Wolfspeed, Onsemi, Infineon |

|

Modular

AI clusters / chips |

Supermicro, Lambda Labs, Tenstorrent |

|

Network

and edge infrastructure |

Arista

Networks, Juniper,

Cisco |

|

Power

redundancy & battery systems |

Energizer, Enersys, Tesla

Megapacks (via Tesla) |

Narrative Risk: As these alternatives rise, investor attention and capital may rotate quicker that the current narrative is “pricing in”.

Positioning Risk: Vertiv may be early AI infrastructure, but not durable AI infrastructure. If thermal/power systems are commoditized, narrative leadership could fade.

2. Lessons from Past Tech Cycles: Infrastructure winners can lose the spotlight VERY quickly

In the 2000s and 2010s, several cycles saw infrastructure players ride investor enthusiasm-only to be re-rated harshly as the cycles matured:

Historical Analogues:

|

Cycle |

“Picks and Shovels” Names |

What Went Wrong |

|

Dot-com

buildout (1997–2001) |

Lucent,

Nortel, JDS Uniphase |

Overbuilt

capacity, weak pricing power, vendor consolidation |

|

Smartphone

revolution (2008–2014) |

Corning,

Texas Instruments (non-core), MEMS sensor players |

OEM

dominance eroded supplier pricing, commoditization |

|

Cloud

infrastructure (2015–2019) |

Seagate,

Western Digital, NetApp |

Transition

to SSD/cloud-native hurt traditional infra margins |

|

Crypto

mining boom (2021) |

Bitmain,

Riot Platforms (infra), Canaan |

Collapse

in ASIC demand, over-reliance on one vertical |

Parallel to Vertiv: In each case, infrastructure names benefited from the early-stage hype, but suffered once demand normalized or OEMs consolidated suppliers. Narrative leadership moved to the next bottleneck in the supply chain.

3. Valuation Assumes Uninterrupted Execution and Margin Expansion

Vertiv is priced for operating leverage, but Q2 margins (~18.5%) declined sequentially. Though management attributes this to timing and mix, margin upside may be near its ceiling:

- Tariff drag, labor costs, and product customization risks

- Integration complexity from M&A (e.g., OneCore, Great Lakes)

- Cyclical deflation in input costs may reverse as inflation eases

Valuation Risk: At current multiples, even 100–200bps margin miss would cause a sharp EPS revision and re-rating.

Multiples are elevated relative to peers and Vertiv's own trading history

4. Backlog ≠ Contractual Revenue

Vertiv’s $8.5B+ backlog is impressive, but not all of it is contractually locked or near conversion. Key risks include:

- Scope changes or redesigns by hyperscalers

- Delays in permitting or grid interconnects

- Project cancellations if AI ROI disappoints

Signal Risk: Book-to-bill ratio and backlog burn will be watched closely-especially how they pan out into 2026.

5. Execution Complexity at Scale

The very things that drive the bull case—global footprint, modular expansion, vertical integration, also increase fragility:

- Small missteps (e.g., in Mexico, APAC, or Europe) can cascade through the system

- Aggressive delivery cycles in AI projects heighten logistical risks

- Warranty/service issues on new product lines may emerge over time

Execution Drag: Managing this complexity while maintaining margin expansion will not be easy.

Technical check- stock at all time high would be tough to sell. There are no signs of weakness on the charts as yet.

Final Thought

Vertiv is a credible AI infrastructure play today. But every cycle reveals new bottlenecks, and narratives evolve. As new “picks and shovels” emerge-whether in optics, power semis, or edge computing the market’s focus may shift (quickly!).

The history of tech investing suggests this:

Being early and critical doesn’t guarantee being durable or irreplaceable.

Vertiv’s current valuation implies the infrastructure premium will last years. But what if it doesn’t?

Investor’s Checklist

· Monitor rotation to new “infra” stories in AI (e.g., optics, cooling, broader semis)

· Track book-to-bill and margin trends closely-especially going into 2026

· Stress-test DCF using flat vs. declining margin scenarios

· Evaluate customer concentration and contract terms in the backlog

· Compare Vertiv’s valuation against both peers (and successors) in the “AI stack”

Bottom Line

|

Strengths |

Challenge Areas |

|

High

exposure to AI data center buildout |

History

suggests “picks & shovels” leaders often rotate |

|

Strong

orders and expanding product lines |

New

competitors (optics, cooling, power semis) emerging fast |

|

Backlog

supports near-term visibility |

Conversion

risk, delays, and scope changes common |

|

Operational

scale post-restructuring |

Execution

risk grows with scale, integration, and product complexity |

|

Tailwinds

from digital infrastructure |

Valuation

assumes uninterrupted, multi-year compounding |

Member discussion